While tax deductions are available to Long-Term Care Insurance owners the particulars point to a decision between modest tax savings today versus more significant tax savings in the long run.

If we’re honest, there are two things that most people don’t want to spend their hard-earned assets on: Taxes and insurance premiums. That said, the downside risk of not paying either of those expenses is severe enough to motivate many to not only pay their taxes, but also take some risk off the table beyond home, auto, health and life insurance. As an example, Long-Term Care insurance has become another necessity for anyone wanting a high degree of control regarding how they receive care as they age.

That said, Long-Term Care insurance represents one of those rare instances where paying insurance premiums can actually reduce your tax bill. Exactly how to go about achieving those savings will depend on the nature of the coverage as well as the particulars of the client’s tax planning.

In terms of the coverage, there are four factors what will impact how to take a deduction and the size of that deduction:

- The insurance product must fall under section 7702(b) of the internal revenue code.

- It also has to have separate charges related to the acceleration of benefits, continuation of benefits and any inflation protection, as well as no cash value related to these elements of the product. Together, this generally eliminates all the Long-Term Care riders available on traditional life insurance products.

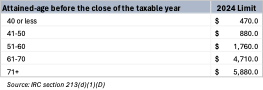

- There are age-based limits to how much a client can deduct. See Table 1 for additional details.

- The client must itemize, and their total medical expenses have to exceed 7.5% of AGI

Table 1

Itemized Deduction Example:

- Male, age 55:

- Annual LTC premium: $5,000

- Age-based limit: $1,760

- Deduction = $1,760

- Female, age 72:

- Annual LTC premium: $5,000

- Age-based limit: $5,580

- Deduction = $5,000

All the factors listed above prevent many from deducting any of these charges. Fortunately, there is another path for individuals to achieve a similar outcome. If their health insurance coverage includes a Health Savings Account (HSA), the most significant barrier from the list above comes off the table: The need to itemize their taxes.

HSA participants can use their HSA assets to pay the portion of their Long-Term Care Insurance premium attributable to the actual coverage using the same guidelines list above, capped by the age-based limit. Of course, if the client is already max-funding their HSA, then they can simply pay as much of their premium as the age-based limit will allow from those assets, preserving their earned income for other purposes. If they’re not fully funding, however, increasing up their contribution with the express purpose of using those funds to pay their LTC premium is the most straightforward way to achieve a deduction.

There are, however, a number of additional considerations to keep in mind: It may be in the client’s best interest in the long run to let those HSA funds grow versus using them to pay premiums. Long-Term Care costs are not the only costs that rise as the years go by. Out of pocket expenditures increase as well. Further, preserving those HSA funds to pay for treatments that may not be covered by health insurance despite being an appropriate treatment option is also a strategy worth considering.

What’s the bottom line?

Ultimately, there is no single right answer here. If the client is a bit older and itemizes, simply taking the deduction via itemization is a clear winner. Beyond that, it is admittedly a bit more complicated. For clients participating in an HSA or with a seasoned HSA from prior participation, using these funds is a viable tax minimization strategy that should be considered based on not only the particulars mentioned above, but also the balance of their tax planning. In addition, the decision regarding how to pay premiums my vary from year to year as well.

The real advantage of the entire conversation is that these strategies can make Long-Term Care Insurance more affordable, rendering coverage more accessible. In addition, while it is beyond the scope of this discussion, business owners have more tax-advantaged premium payment options available to them, as do employees with access to coverage through their benefits program.