A well-crafted and effective estate plan will often span generations. Implementing insurance solutions involving later generations who may not have a significant net worth today, however, can be challenging. The impending sunset of the Tax Cuts and Jobs Act at the end of 2025 increases the risk that comes with waiting until receipt of an inheritance to implement an estate plan.

One of the keys to preserving family wealth across generations is designing and implementing estate plans that involve younger generations of the family. Not only does this create the cohesion required for these plans to be maximally effective, but it also allows insurance solutions to be put in place far earlier than might otherwise be possible. In doing so, it can also address some of the challenges presented by insurability at older ages, easing the sting of a lack of insurability in G1, and/or placing insurance on G2 before their health presents a problem. Additionally, the impending sunset of the Tax Cuts and Jobs Act (TCJA) makes multi-generational planning all the more important as a strategy for addressing uncertainty about the future of estate tax exclusion amounts. All of that said, insurance companies can often be reluctant to approve and issue large insurance policies based on future events that may or may not come to pass. Successfully navigating this process requires a higher degree of specificity and plan documentation, reasonable growth assumptions, and an insurance underwriter with a clear understanding of the wealth transfer market.

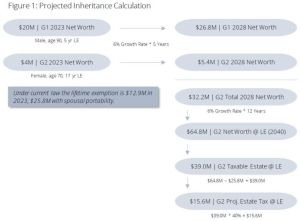

Those ingredients serve to document G2’s projected net worth at their life expectancy and justify the insurance amount required to meet the corresponding future estate tax liability. A “safe harbor” of sorts for this calculation involves taking G2’s current net worth, inclusive of the projected inheritance, growing at 6% to the client’s life expectancy.

The projected estate subject to tax is then calculated and multiplied by 40% to arrive at the required amount of insurance. The calculation described above must be supported by additional documentation that meet the financial underwriting requirements of the carrier underwriting the application. See Figure 1, Projected Inheritance Calculation, for additional details.

The result in this instance is an insurance need of $15.6M, an amount far in excess of G2’s current net worth. Placing that amount of coverage would be quite challenging without a well thought out process and a carrier who views estate planning in the same manner as the client and their advisors. In addition, the keen observer will note that the calculation in Figure 1 is based on today’s estate tax law despite the fact the Tax Cuts and Jobs Act will expire at the end of 2025 absent action by Congress. This approach of using current law despite what changes the future may hold has been insurance company policy for quite some time. Rather than attempt to forecast what could happen, most will simply assume current law will be on the books forever. That underwriting approach cuts both ways, either helping or hindering planning efforts depending on the current law.

The challenge presented by today’s legislation and what is at best a 50/50 proposition in terms of an extension of the limits under the TCJA would leave a client like the one in our example with an even larger tax exposure. That possibility drives home the need for this type of planning. If, for instance, the TCJA does sunset at the end of 2025, G2’s projected estate tax could balloon to something in the realm of $21M. For clients who have executed this type of planning, that translates to a need for $6M in additional insurance. For those who have done no planning, that amount jumps to over $21M, increasing the risks associated with failing to act now dramatically.