There’s a lot of potential change on the horizon in the Long-Term Care and Estate Planning markets. Between a potential wave of state level LTC legislation plus the possible sunset of the estate tax exclusion levels embedded in the Tax Cuts and Jobs Act (TCJA), clients are facing a period of uncertainty than can have real consequences over the balance of the decade and beyond.

As important as both of those potential planning challenges are, the largest risk clients are facing is the very real need to have a plan for care in place as they age that includes both how they want to receive care as well as how to pay for it. Many are feeling this rather acutely as they care for their own aging parents.

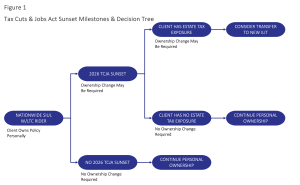

For clients who may find themselves subject to estate tax if current estate tax exclusion limits expire, their Long-Term Care strategy needs to be flexible enough to not only position them to take advantage of any possible opt-out of state level LTC programs, but also address the potential TCJA sunset. It likely also involves pushing some of this risk off to the experts: Insurance companies. A well-conceived and executed solution will:

- Use the most cost-effective strategy to secure Long-Term Care coverage

- Allow for “ownership optimization” of the coverage in the event of the TCJA sunset that creates an estate tax liability

The primary objective is to provide robust LTC benefits as efficiently as possible. Assuming the client has beneficiaries, a life insurance solution likely offers the best value, with either the client or their loved ones receiving significant benefits. At the same time, the use of a joint life product that accumulates cash provides additional efficiency and flexibility.

- Fund a Survivorship IUL (SIUL) policy with LTC rider:

- Covers both insureds with an individual pool of LTC

- Provides Indemnity benefits

- Offers a potential return on premiums instead of simply return of premium

- Establishes or enhances a significant legacy if not needed for care

- When/If the client has future estate tax exposure:

- Transfer ownership of the coverage to the client’s newly established ILIT. This reduces their taxable estate once the look-back period expires

- Utilize trust language that allows access to LTC benefits during their lifetime. If there is a claim, this could remove additional assets from the client’s estate

For a pair of 55-year-olds, both in Preferred health, a properly-funded $1MM SIUL policy with a total LTC pool of $500K each has an annual premium of $10,890, well within the annual exclusion gift limit. If none of the risks we are seeking to hedge actually come to pass, their beneficiaries receive the proceeds. The tax-equivalent IRR on the proceeds assuming the clients pass at age 90 is 6.06%.*

The other question is what happens if they need care? If both clients exhaust their benefits during their lifetime, the IRR may increase given they would likely receive these benefits earlier in life.

How does the Hedge Play out?

Potential LTC Legislation

In the event the client’s state of residence enacts LTC legislation with an opt-out provision triggered by existing LTC coverage ownership, the clients may be eligible based on the true 7702B LTC benefits included in the policy. While the specifics of any future legislation are obviously unknown, it is possible that Chronic Illness Benefits under section 101(g) may not qualify for opt-out, making 7702B products a safe harbor of sorts.

Additionally, given that the final form of any legislation is yet to be specified, the ability to opt out and the requirements to do so are unknown at this time. This makes it critical to focus on the planning need first, with the goal of opting out of any future legislation as a possibility rather than the sole driver of the purchase of LTC coverage. A review of any proposed legislation in the client’s state of residence as part of the planning process is essential.

Potential Sunset of the Tax Cuts and Jobs Act

The only thing we know about the future of estate taxation, based on history, is that there will be change. In the event the client finds themselves with an unexpected estate tax exposure resulting from future changes, establishing an ILIT and subsequently transferring ownership of the policy to the ILIT removes the death benefit from their taxable estate after the look back period expires. The use of indemnity benefits on the Nationwide policy also unlocks an extremely estate tax friendly way to manage the benefits, that can remove additional assets equivalent to the benefits received plus interest from the client’s taxable estate. Please see Figure 1, below for additional details on this element of the strategy.

Unlocking the “Extra” Estate Tax Exclusion

Client Needs Long-Term Care

- Client buys $1MM life policy with LTC rider in their ILIT using funds earmarked for LTC

- Carrier pays indemnity LTC benefit to the trust ($20K/month for 50 months)

- Client borrows funds from trust to pay for LTC expenses

- Interest is capitalized annually

- The client passes away at exhaustion of benefits

- LTC Benefits Paid: $1,000,000

- Accrued Interest: $220,000

- Estate Debt to Trust: $1,220,000

At Client’s Death

- Estate Repays the Loan

- Total Amount in Trust: $1,220,000

Additional Details

- Trust Language must allow for LTC ownership as well as loans to the Grantor.

- Not all Insurance Companies allow their LTC products to be owned in an ILIT.

- There are very specific technical requirements for the loan to the Grantor.